550+ customers targeted by 0 successful fraud events

190 Countries

The largest coverage of international bank accounts on the market

3X Faster

No more manual callbacks, vendor controls are automated

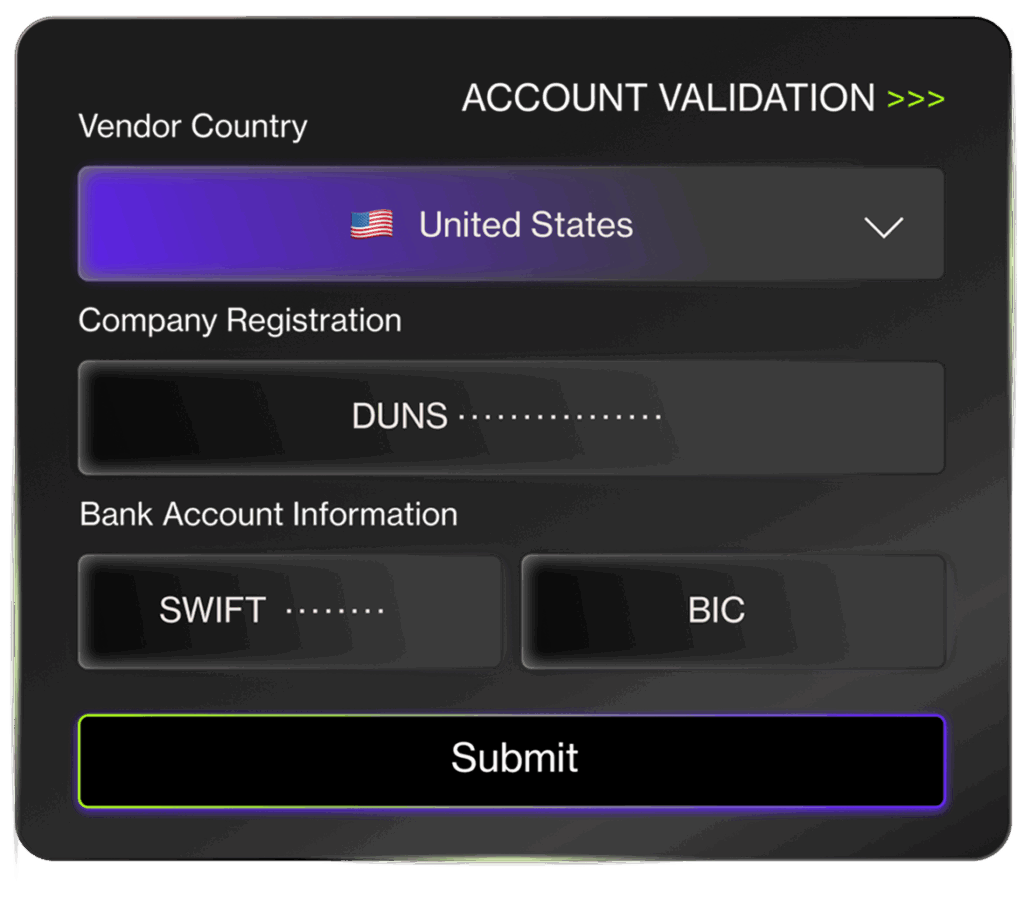

Instant And Automated Bank Account Validation

Calls, counter-calls, emails: manual vendor account validations performed by financial teams are vulnerable to fraudulent transactions. Manual, time-consuming, and highly fallible, a single control takes over 30 minutes on average. With Trustpair’s services:

Confidently validate vendor bank accounts worldwide (190 countries)

Boost team efficiency and stop draining resources through automation

Get instant evaluations with contextualized assessments for 90% of validations

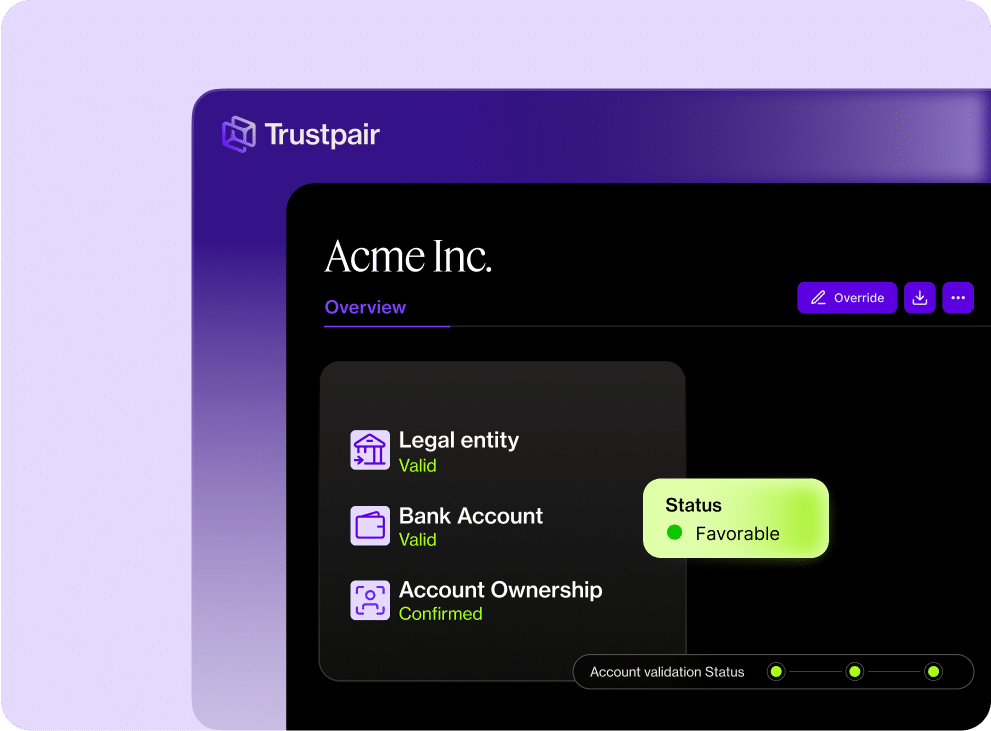

International Account Ownership Verifications

Verifying account ownership internationally is not a simple task for Finance teams. Many tools only allow domestic validations. With Trustpair, access automated instant account validations worldwide and guarantee international vendor data quality and legitimacy.

Billions of bank accounts verified in 190 countries

The most comprehensive network of bank account databases

1000+ leading financial institutions in the network

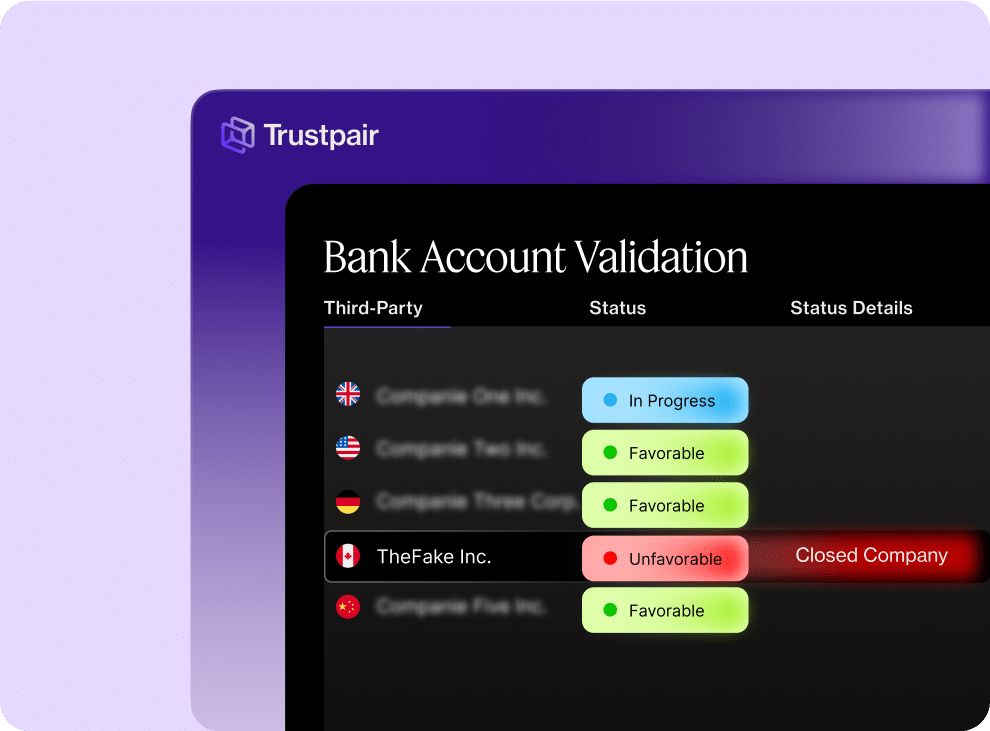

Simple And Automated Account Validation Process

From vendor onboarding to payment execution, Trustpair automates every step of the account validation process. Seamless, instantaneous, and fully integrated, the solution fits directly into your existing financial workflows with no manual effort required. With Trustpair:

Connect instantly to your ERP, TMS, or procurement platform through native integrations with SAP, Oracle, ION, Ivalua and more

Verify in real time every bank account against a network of 1,000+ financial institutions across +190 countries

Stay protected continuously with automated monitoring that flags any suspicious change before a payment is released

Compliance With NACHA And International Regulations

Verifying account ownership isn’t just about payment fraud prevention. It helps businesses meet domestic and international standards, avoid penalties, and secure transactions. Account validation enables organizations to comply with key regulations, including:

NACHA (WEB Debit Account Validation Rule): Requires businesses to validate routing and account numbers for ACH payments made online – ensuring the account is legitimate before transactions.

Anti-Money Laundering (AML) Regulations: Verifying account ownership supports Know Your Customer (KYC) and Know Your Business (KYB) obligations, helping to prevent the use of fraudulent or misrepresented accounts.

International Frameworks (e.g., FATF, PSD2): For multinational businesses, account validation also supports compliance with international best practices for secure cross-border payments and AML requirements.

What are the best strategies for effective account validation?

The best strategies for account validation combines compliance, consistency, and strong due diligence. Companies should align with financial regulations, standardize their internal processes, and use tools for automated account validation.

Comply with regulations

Frameworks like Nacha (for ACH payments), KYC (Know Your Customer), and AML (Anti-Money Laundering) set clear standards for safe account validation. Following these rules helps prevent payment fraud, money laundering, and terrorism financing. It also protects customer data and builds trust with partners.

Standardize your processes

Account validation is most effective when it’s consistent. Standardization reduces manual errors and ensures controls are applied throughout the vendor lifecycle. Best practices include:

Apply clear checks for new suppliers

Validate bank accounts regularly

Keep an audit trail for regulatory requirements

Do your due diligence

Account validation should go beyond compliance. It’s a fraud prevention tool that confirms account ownership and detects identity fraud before payments are made. Enhanced due diligence is possible with automated solutions like Trustpair, which runs systematic, real-time checks and continuously monitors vendor data to flag suspicious changes.

Is validating routing numbers enough to prevent payment fraud?

Validating routing numbers confirms the bank and branch, but not the account ownership. On its own, it cannot prevent fraud.

Full account validation is needed to confirm account information and verify legitimacy through an identity verification process. Without this, businesses risk payment failures, identity fraud, and gaps in regulatory compliance.

Many companies now use automated account validation tools, like Trustpair, to check bank accounts in real time. This approach strengthens fraud prevention and ensures every transaction is accurate and secure.

What are the risks of not validating account information?

Not validating account information exposes companies to legal, operational, and fraud risks. Without proper checks, organizations face compliance breaches, payment failures, and exposure to identity fraud.

Legal Risks: Failing to verify accounts can lead to non-compliance with US laws such as Nacha, KYC, AML, and SOX. This may result in corporate fines and legal issues during audits, especially for publicly traded companies.

Operational Risks: Without account verification, businesses face increased chances of errors in banking details and transactions. These mistakes can damage supplier relationships and often result in irreversible fund transfers.

Fraud Risks: Lack of account validation exposes businesses to various fraud schemes. Common techniques include vendor fraud, phishing attacks, and CEO impersonation. Scammers may use spoofing, false invoices, or network hacking to commit fraud.

What are the benefits of instant verification?

Instant account verification lets companies confirm bank accounts and account ownership in real time. It removes delays from manual verification, reduces errors, and helps organizations comply with financial regulations. Trustpair offers an ultimate solution to secure the vendor onboarding process through its automated account validation system.

The biggest benefit is stronger fraud prevention. By leveraging Trustpair’s comprehensive banking data sources and smart algorithms, companies can instantly verify vendor bank account details across 200+ countries. This automated validation not only saves time but also eliminates human error, ensuring that every new vendor is thoroughly vetted before being added to the system.

Key benefits include:

Faster onboarding and smoother payment processes.

More accurate account information with fewer payment errors.

Better compliance with anti money laundering rules and regulatory requirements.

With Trustpair, organizations can confidently establish secure vendor relationships from the start, minimizing the risk of fraudulent activities throughout the entire business relationship.

How to implement real-time account validation?

To implement real-time account validation, integrate automated bank account verification directly into your ERP, procurement, or payment systems so account details are checked instantly before payments are released.

The most effective approach is to use fraud prevention software that offers native integrations with your existing tools, ensuring continuous and automatic validation without manual intervention. Solutions like

Trustpair enable real-time verification of vendor bank details, reducing payment fraud risk while keeping finance workflows efficient.

What are the risks of manual account validation?

Relying on manual bank account validation creates serious challenges. It slows down processes, increases human error, and leaves room for fraud.

Key risks include:

Errors and payment failures: Manual checks of account information are prone to mistakes, leading to failed payments or lost funds.

Weak fraud prevention: Without automated checks, companies are exposed to identity fraud, vendor impersonation, and money laundering attempts.

Compliance gaps: Manual methods rarely meet today’s strict regulatory requirements such as KYC and anti money laundering rules.

Many organizations use solutions such as Trustpair to automate these checks and keep vendor data secure.

Account validation software RFP: which solutions should companies reach out to?

Enterprise organizations handling high volumes of supplier payments should reach out to solutions purpose-built for payment fraud prevention like Trustpair. Trustpair provides automated bank account validation and continuous monitoring of supplier banking data, with global coverage in 190 countries and native integrations with major ERP, TMS and procurement platforms such as SAP, Oracle, ION and Ivalua, helping prevent fraud before payments are executed.

When issuing an RFP, companies should evaluate bank account verification software based on automation, data reliability, system integration, scalability, and its ability to reduce fraud risk upstream in the payment process.

TESTIMONIALS

Voices of Trust

Explore how our solutions have empowered businesses like yours to fortify against fraud and build a resilient financial ecosystem.

Mauro Portela

GBS - Managing Director Global MDM Operations

"Thanks to Trustpair, we've made a significant shift in our security processes and filled the gaps we needed to fill. Trustpair has proved to be a committed and trustful partner and we've appreciated the support and transparency."

Michele Bruno

CFO and Treasurer

"With Trustpair's verification methodology, it's no longer just a consistency check but an exact confirmation of the validity of the third party: There is no longer any risk."

Monika Razny

Treasury and Corporate Finance Manager

"We've gone from manual and time-consuming fraud controls to automated bank account validation done directly in SAP. The workload has been drastically reduced and payment security is now guaranteed."

Malika Benfares

Head of Treasury and Consolidation

"Trustpair protects all the payment chain, reassures employees of their responsibility and makes the managers aware of the risks."

Joffrey Tabouret

Head of Treasury and Financing

"With Trustpair, we are able to automatically and quickly monitor our third parties and ensure the security of that very data over the long term"

Fabrice Meunier

Administrative and Financial Manager

"I would definitely recommend Trustpair to finance departments. It makes adding and modifying beneficiaries more reliable, without resorting to manual processes that are cumbersome, time-consuming and fallible."

Fanny Harquel

Accountability Manager

"The control process is simplified with the Trustpair solution, the Finance Department is reassured and, above all, it no longer needs to waste time performing manual checks to verify a supplier's bank details."

Colin Cesena

Middle Office Treasury Manager

"Trustpair adapts very well to the specifics of our market and our way of working. Several features are developed as we work together. That's a real plus."

Etienne Mechain

Financial Manager

"Trustpair has become more than a reflex; it has become an obligation. The team no longer validates an IBAN unless Trustpair has confirmed it to us."

Patricia Y.

Director, Global Procurement, Enterprise(> 1000 emp.)

"Trustpair effectively validates bank account ownership for vendors requesting bank changes, which aids in fraud prevention. I also appreciate the coverage that Trustpair provides."

Paweł S.

Master Data Manager, Enterprise(> 1000 emp.)

"What we value most about Trustpair is its ease of use and ability to provide clear risk insights. It enables us to focus on critical areas, streamline fraud prevention, and maintain compliance worldwide. The platform’s global reach and integration capabilities make it an essential part of our financial security strategy."

Fatiha B.

AP Manager, Mid-Market (51-1000 emp.)

"An easy-to-use tool, international scope on controls, speed, reliability. A team attentive to clients, responsive and creative."

AJ A.

Master Data Manager, Enterprise(> 1000 emp.)

"Flawless security, Great Automation and Support."

Claire S.

Supplier Risk and Compliance Analyst

"Ease of use, implementation, features and customer support."

Christian V.

Treasury Manager, Enterprise(> 1000 emp.)

"The Trustpair solution secures financial transfers, with ease of use and proven efficiency."

2026 Fraud Trends - AI Fraud Outpacing Human Defenses